A Star worth a Touch ($TST.L)

A Star worth a Touch ($TST.L)

Touchstar plc - a stock too cheap to ignore

I am not an accredited financial advisor. The content on this substack is my personal opinion and not financial advice. Please do your own research and consult a professional before making investment decisions. If you invest in stocks, consider using limit orders. Invest responsibly.

Market-Cap: ~7m

Debt: nil

Enterprise Value: ~4.4m

EBITDA: 1.3m

Free Cashflow: normalised 0.7m

Outstanding Shares: 8.2m

TL;DR

Touchstar, formerly Belgravium Technologies plc, caught my attention because the stock is just too cheap to ignore.

While a low valuation might just reflect the fundamentals of a low quality business, I think Touchstar’s fundamentals are actually of decent quality. This is in part the result of a transformation which has been kicked-off back in 2018.

This quality is reflected in the company (today) ...

providing mission-critical and very sticky hard- and software solutions

comprising 4 complementary business divisions with cross-sell potential

being led by a talented capital allocator (10% holder) for the last 9 years

having 40% recurring revenues that will increase further

being cash-generative with FCF sitting between 0.5m and 1m a year

All of this is undermined by zero long-term debt, ~3m net-cash, 30% total insider-ownership and a dirt-cheap multiple of 3.6 x EBITDA and 4-8 x FCF (depending on how you normalise it).

So where’s the catch?

Either way, this is very cheap. So where’s the catch?

Well, based on my research I couldn’t find (a significant) one. While I generally don’t like write-ups starting with a too simple rationale like “it’s illiquid” or “undiscovered” or “dead-boring” this might actually be one. So sorry for that.

Illiquid Nano-Cap

But let me at least add some color here. With 7m market-cap Touchstar qualifies as nano-cap, the tiniest bracket of listed companies, with no meaningful institutional ownership.

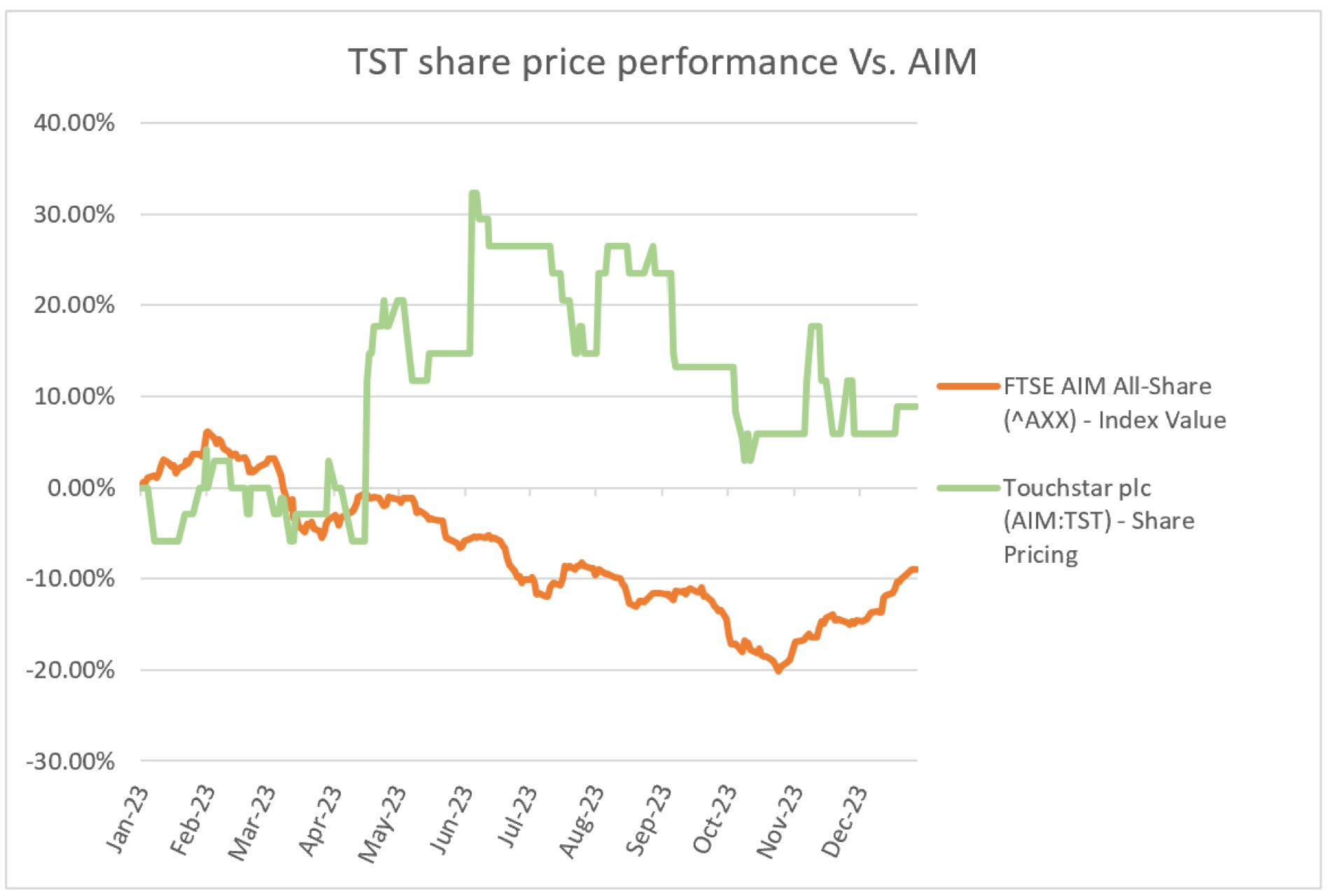

Looking at the order book, only a few thousand shares exchange hands every day indicating that most investors are firm holders. This is further undermined by a negative beta, meaning the stock movements do not align closely to the overall market. Learned this from

- you should follow him.I think the graph below confirms this quite well.

The chart demonstrates something else. If a company moves in the opposite direction to the overall market in times that can be without doubt described as challenging, you may be on to something. In the book “Outsiders CEO” this phenomenon is represented as one key aspect indicating extraordinary management performance.

Spoiler: Touchstar has improved its fundamentals significantly over the last 5 years.

Undiscovered

Further, there are no investor presentations, no earnings calls and the last tweets on Touchstar are dated 5 years back. The author of the tweets was a holder until 2019 and sold out before the stock became more than a double in 5 years time (no finger-pointing here, happened to me recently as well).

“If people are bored, they sell and buy something else.”

It just confirms my view that the company is just too boring with little share-price fluctuations so sitting on one’s hands might be difficult here. The stock was never a rocket-ship and who even reads a thesis for prospective 20% returns a year? If people are bored, they sell and buy something else.

Valuation & est. Upside

My thesis isn’t based on “it should be at least 6 x EBITDA” because I am not able to predict whether Mr. Market will do this for us.

My assumption is simply that the company amasses similar amounts of cash compared to previous years for the next 5 years. I did not account for meaningful revenue acceleration nor further improving fundamentals (in terms of margins)and so I did not account for multiple expansion either. Find below the operating cashflow from 2019 - 2023 (l-t-r).

If that, in my opinion conservative assumption, holds true, the free cash generated will about to equal today’s market-cap in 5 years to come. Assuming the same ridiculous valuation (40% net-cash) in 5 years time (it will be still a tiny company then!) the stock would be at least +100%, a double from today’s level.

As said, all of this excludes further improving fundamentals, an accelerated revenue growth or a re-rating of the stock based on the higher quality of (recurring) revenues.

However, the upside will be most probably realised by a combination of continued stock buy-backs and dividend payments (as previously done) with extra room for multiple expansion driven by further improving fundamentals. So +100% should be the minimum upside and this fulfills my criteria of 20% CAGR with minimum downside potential.

Downside

Talking about downside. As the company is protected by a high stability of earnings (as demonstrated over the last 5 years), significant portion of recurring revenues, very sticky products & services, no debt and a comfortable net-cash position, I don’t see a significant downside here. This view is confirmed by recent stock buy-backs and dividend payments which seem to be good capital allocation.

A further multiple contraction is highly unlikely at these levels and a downside only possible if fundamentals significantly deteriorate. This could happen due to …

bad working capital management

overspending on R&D Capex not translating into higher revenues or margins

cash burning expansion efforts

non-accretive acquisitions

I will dive into some of these aspects in my write-up. Given the hard work of management over the last 9 years with the main benefits coming to light in recent years I hold none of this for a likely scenario.

And that’s it. Not a TL;DR as you would expect, but my thesis is simple. It doesn’t get more sophisticated, so either move on or enjoy a deep-dive on some topics below.

The Turnaround

In June 2015 Ian Martin (10% insider stake) was appointed chairman of the company and has led a significant business transformation.

Under his oversight Touchstar achieved cost savings through closing of a production/repair facility, reduction in office space, closure of administrative functions and an IT consolidation programme.

Further the company overhauled its offering and expanded to new markets and verticals.

As part of the transformation, Belgravium Technologies plc was renamed as TouchStar plc on the 24th May 2016.

Acceleration through fundraising in 2018

The strategic programme as presented above was accelerated by a fundraising performed in early 2018. The fund-raising resulted in the issuing of 2,166,327 new shares at 60p per share which generated £1,300,000.

It is remarkable that insiders alone subscribed to almost 400k of those shares with Ian Martin subscribing to 333k open offer shares alone.

The proceeds were supposed to …

accelerate growth in revenues

increase proportion of recurring software revenues and

help the company to become a more holistic solutions provider

We have refocused Touchstar to be a business that enables data to be captured, moved and used, which is a good place to be in the modern world. This successful fund raising allows the development and growth of the business to be faster. It is an exciting time for us.

While these initiatives have brought the company back on growth track and increased earnings per share manifold (from negative 0.4p to 7.63p per share) the valuation of the company has never caught up with the higher quality of the business as it stands today.

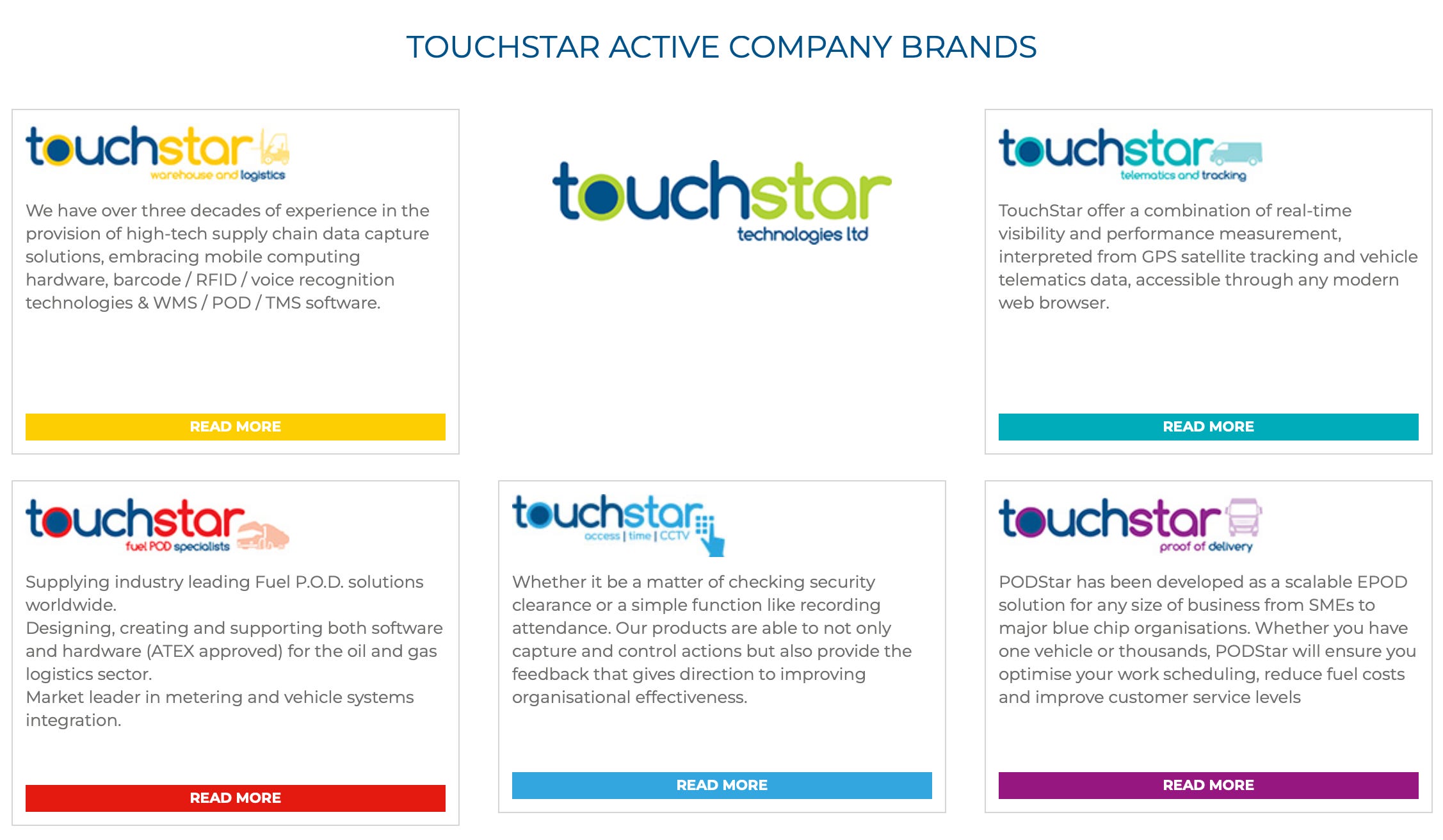

Products & Services

Something I really like about Touchstar is its holistic offering represented by 4 business divisions some of which are complementary and offer a high cross-sell potential. Currently it is not clear, if “warehouse and logistics” is still an active business operation as it was mentioned in one of the filings that a sale was being considered.

The broad portfolio results in multiple revenue streams including software licenses and subscriptions providing for continued improvements in revenue run-rate and stability of earnings.

Electronic Proof-Of-Delivery (POD) - A software suite

PODStar with POD being an acronym for Proof-Of-Delivery is a software enabling fleet operators to obtain an electronic proof of delivery confirming receipt of the goods or services delivered.

This proof is immediately sent to the back-office allowing for timely invoicing and therefore maximising cashflow for the sender of goods or services.

PODStar has now been further enhanced to cater for the fuel delivery sector, a market in which Touchstar has major clients for more than 30 years. This new product was branded as Fuelstar and is basically a PODStar adaption for the oil & gas logistics sector.

Rugged Mobile Computers - The devices for the software

Touchstar designs, develops and manufactures rugged mobile computers as handhelds, truck mounts, wearables or in-vehicle devices for a variety of demanding sectors like manufacturing, warehousing, cold storage and transportation and logistics.

These mobile devices are built to last and feature a tough chassis ensuring full protection from vibration or shocks. The devices are used for mobile data capture and -management in the sectors above where accuracy and physical protection is key.

For example the Rugged ATEX Certified reads various data streams and combines a tachograph, flow metre, valve control, telematics systems and printer – into one driver-friendly system which feeds information back to the back-office.

ATEX consists of two EU directives describing what equipment and work environment is allowed in an environment with an explosive atmosphere.

Telematics & Tracking

Touchstar’s tracking system provides real-time location monitoring using GPS satellite data, showing individual vehicle positions in real time on a ‘live data’ map. The system enables fleet coordinators to …

See where your vehicles or trailers are heading next including their ETA

Set geo-fences around depots or sites to alert on incoming vehicles

Drill down into specific route analysis information for individual vehicles

Analyze different activities using business intelligence graphics

The solution also helps to optimise driver behaviour and reduce fuel costs for trucks as driving style reports are generated and used for debriefing of drivers.

Access Control - Security Hardware & Evolution Access Control Software

Evolution provides a complete and integrated access control software solution that efficiently captures, monitors, and controls access rights.

EvoLink can link front end software to almost any other system, from HR and Payroll through to cashless vending and other third-party systems where the same personal data is required.

Stickiness & Replacement Cycles

What I like about Touchstar’s products is that they are very sticky.

Rugged Mobile Computers

Imagine how likely it is that a fleet owner managing 100 vehicles would replace its mobile devices in each vehicle even if newer devices were more capable, a bit cheaper in maintenance or had additional features. The effort to replace such a key system would equal a major change of critical infrastructure and would represent a material risk for the ongoing business operations. For products like this the rationale is often “never change a running system”.

Access Control Systems

For access control systems it is similar. This is highlighted in a recent case-study for British Sugar, one of Touchstar’s clients. Touchstar has supported this client’s Access Control System for 20 years after recently having been asked to upgrade it. Long replacement cycles do provide equally long recurring maintenance revenue contracts.

The Crux

However, this is a double-edged sword as selling such mission-critical is also much more difficult and is likely to depend much on replacement cycles. Based on some research I estimate replacement cycles for rugged mobile computers (and software running on it) to be 3-5 years.

This is also confirmed by a note in the FY 23 where Ian highlights that clients are moved to 3- and 5 years billing cycles. This gives additional confidence as I base my investment thesis on the next 5 years. So when the replacement cycle takes 5 years from now it is still early enough to meaningfully kick off revenue growth.

For Access Control System replacement cycles are estimated to be 10-15 years. Yet, access controls systems have not been a key focus of the group in the past so the company is hunting for new opportunities here.

Due to the dependency on rather long replacement cycles, revenue growth will always be a bit lumpy for Touchstar. However, recurring revenues should provide enough stability to ensure a quite smooth revenue run rate over time.

Judging by the numbers

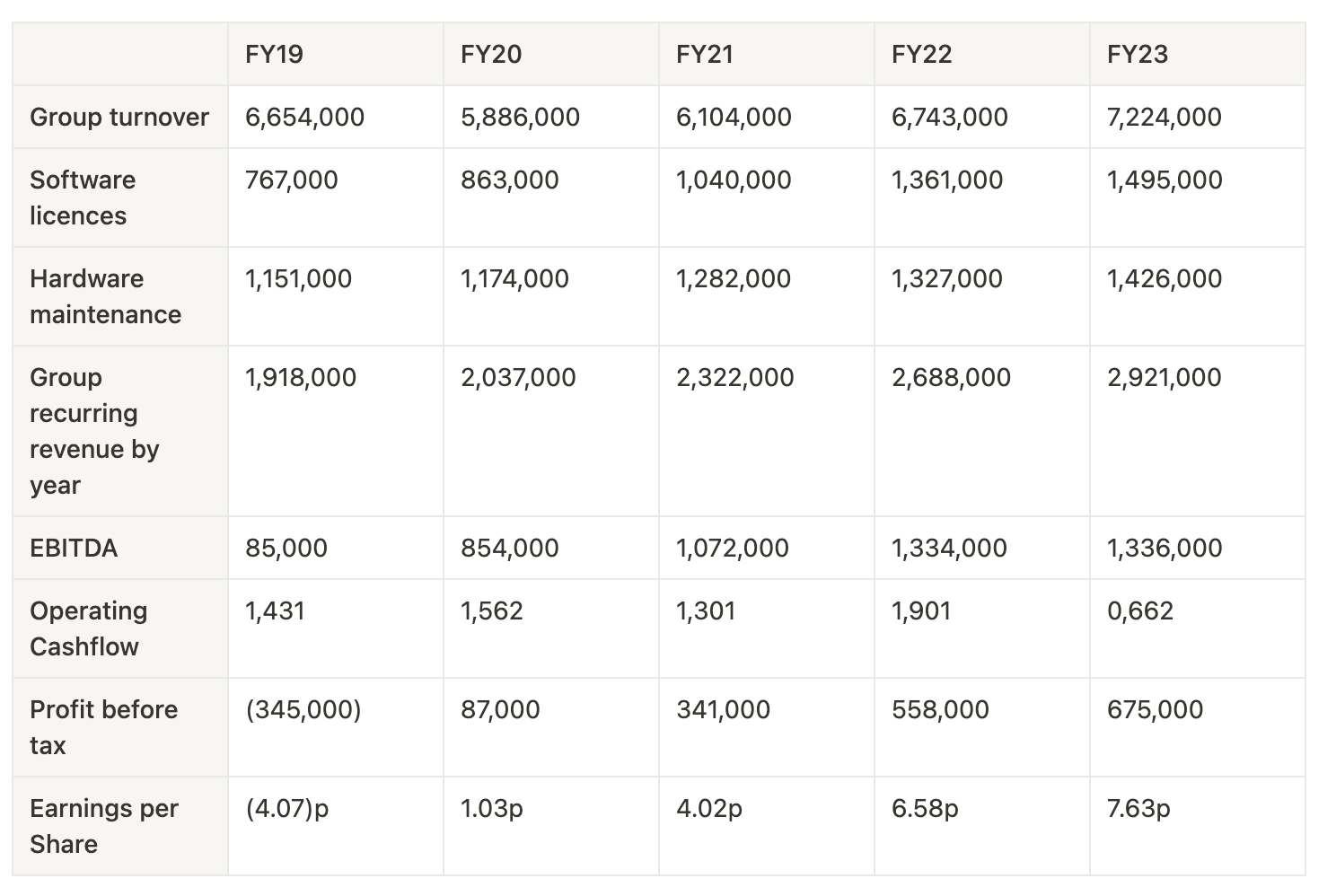

Solid Revenue Growth

Touchstar had made quite some progress in growing its top-line for the last 3 consecutive years. Like for most businesses, FY20 was impacted by Covid-19.

Recurring Software License Growth

Hidden behind the total sales growth is the encouraging, double-digit growth in software license revenues. Over the course of the last 5 years Touchstar has almost doubled software license revenues as demonstrated by a strong CAGR of 20% on average.

Recurring Hardware Maintenance Growth

Equally hidden behind the total sales figure are recurring hardware maintenance services. Despite growing slowly - probably because of its correlation with hardware-sales - it has grown with a 5% CAGR over the last 4 years.

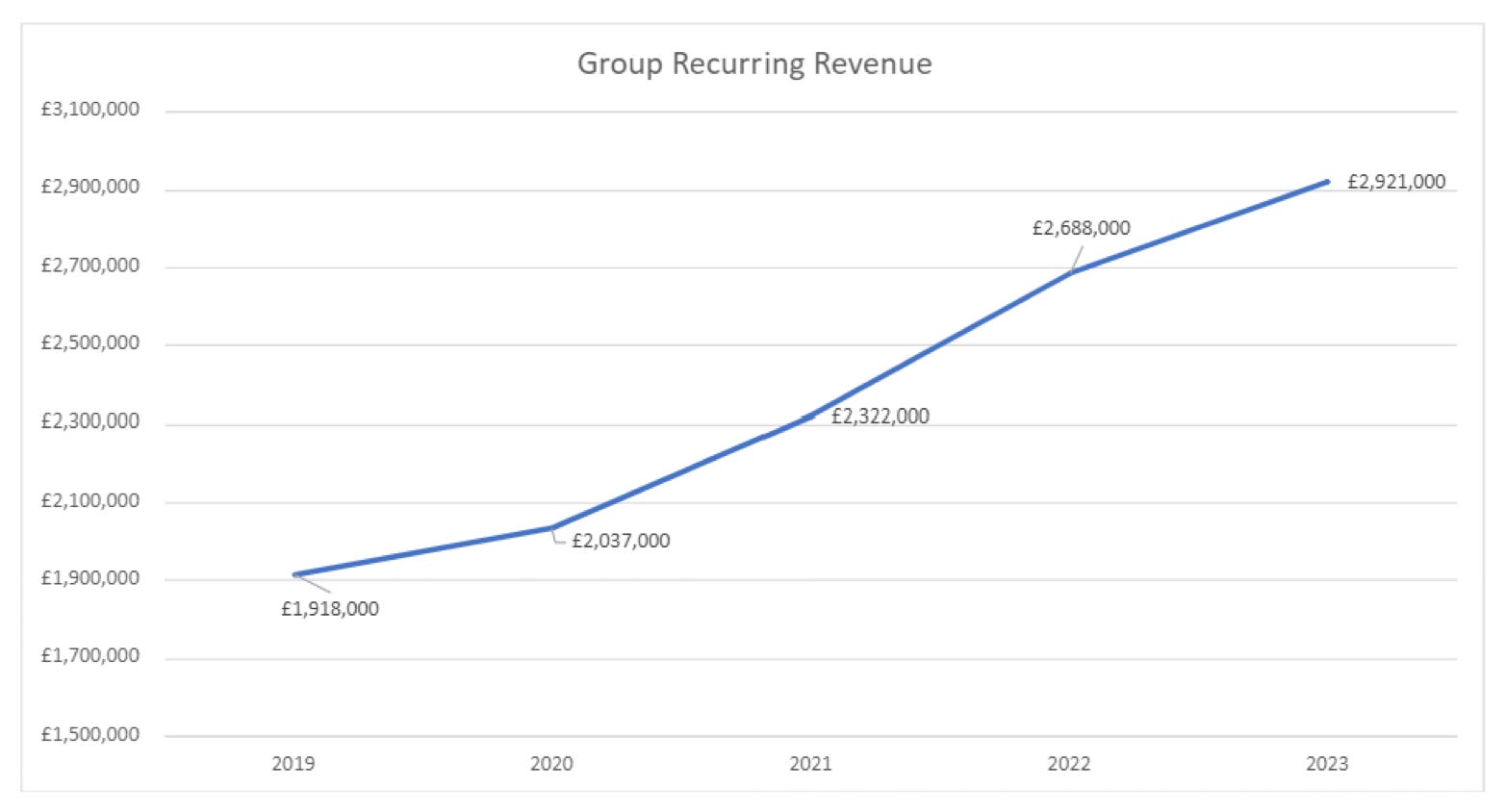

Total Recurring Growth

Recurring software license sales and recurring hardware maintenance sales bring us to total recurring revenue growth. As can be seen below, recurring revenues have increased by around 50% over the last 4 years (~11% CAGR). I expect this further to accelerate as software licenses are now eclipsing hardware maintenance revenues.

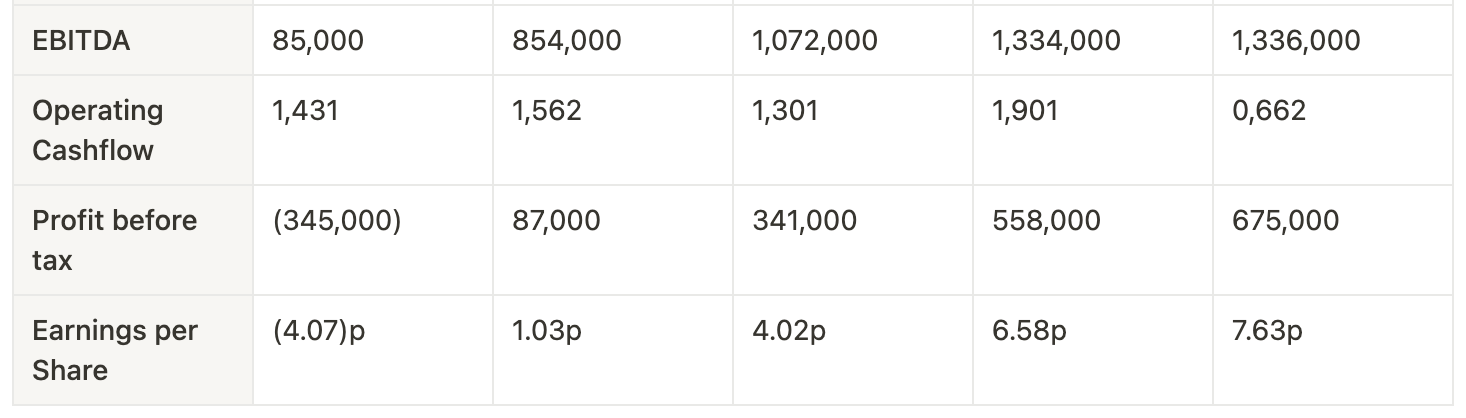

Profitability

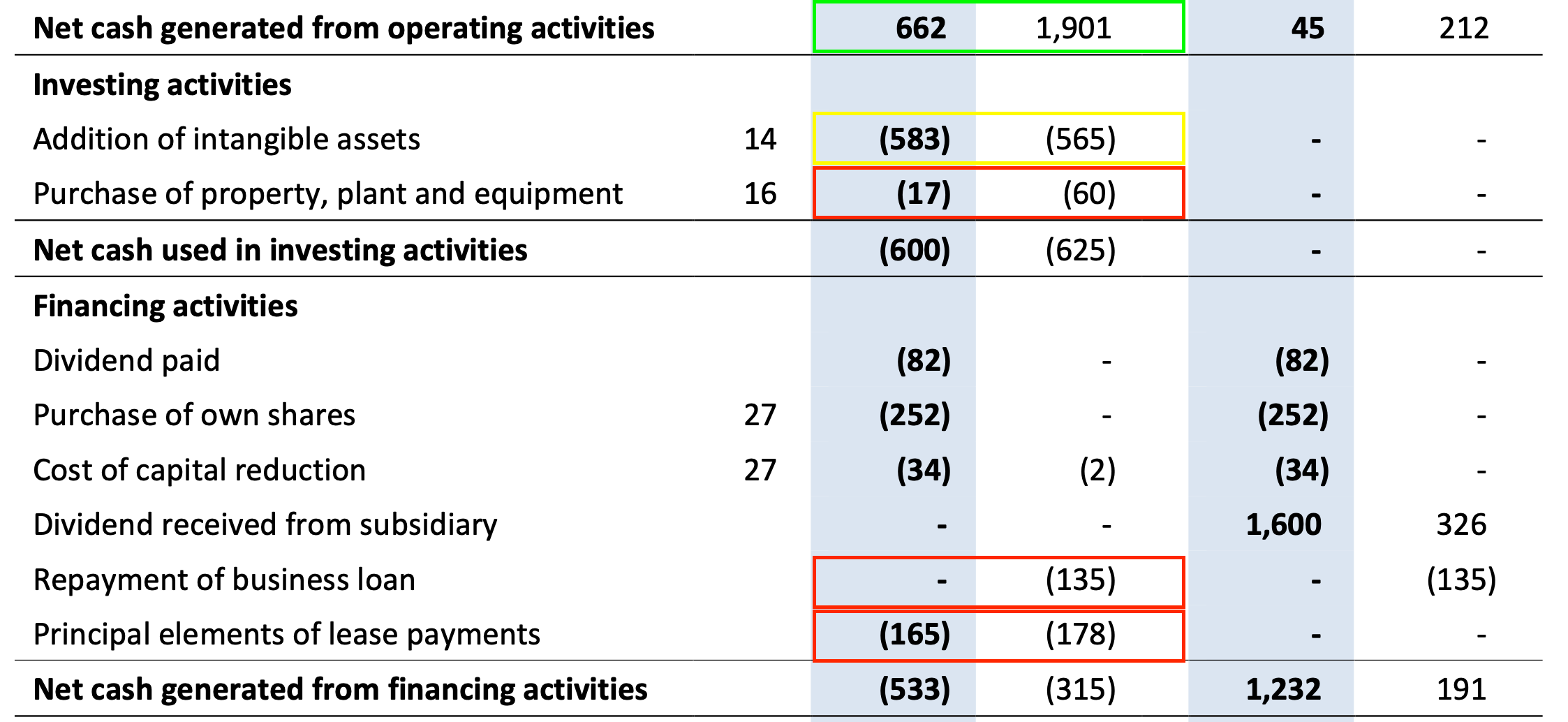

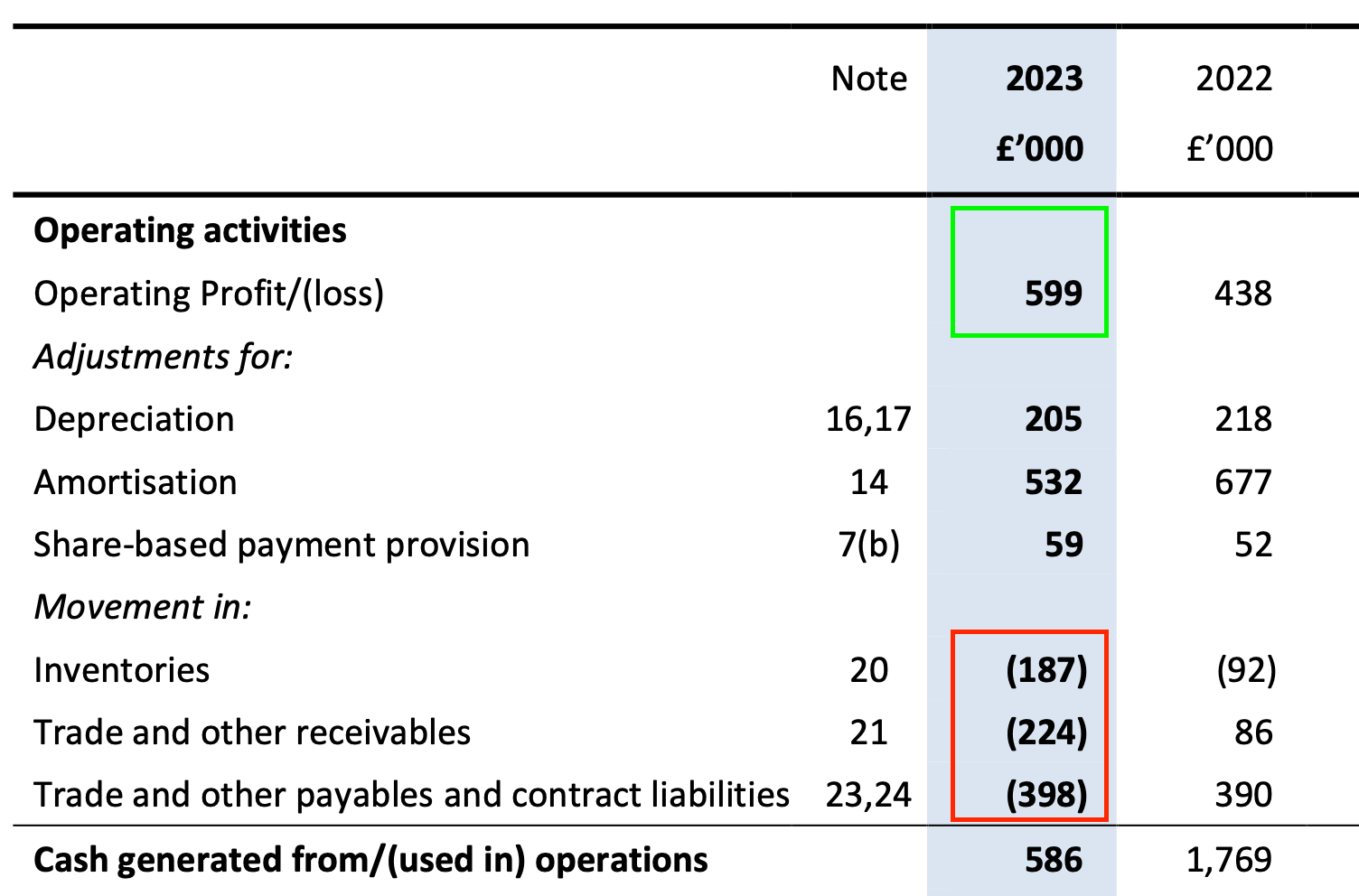

Touchstar has printed a growing EBITDA for the last 5 consecutive years. Note how strong EBITDA converts to operating cashflows. Cashflow for FY24 was lower than anticipated because of working capital movements. Inventory & receivables had a significant increase in the last financial year.

Except last financial year, operating cashflows amounted to well above 1m with very limited capex spend. In-house Software development costs have been in part capitalised so we need to deduct the Capex from Operating Cashflow. The Capex was pretty stable at 0.5m for the last years.

Impressive is the increased earnings per share.

In 2023 Touchstar started buying back stock, a wise capital allocation at current levels.

The company bought back a total of 275,000 shares in 2023 at a total cost of £252,000 ( average cost per share of 91p) reducing the share count from 8,475,277 to 8,200,277.

From the annual report FY23

The Company intends to continue purchasing its own shares, subject to the approval of shareholders at the Annual General Meeting. The Company has again budgeted for up to £300,000 for share buybacks in 2024 although the exact level will be dependent upon availability of shares and the price.

[…]

Our aim is to increase the dividend in line with growth in earnings per share.

EBITDA margins are very solid, amounting to 18%, 19% (2022), 16% (2019) for the last 3 years.

Expansion Efforts

Geographies

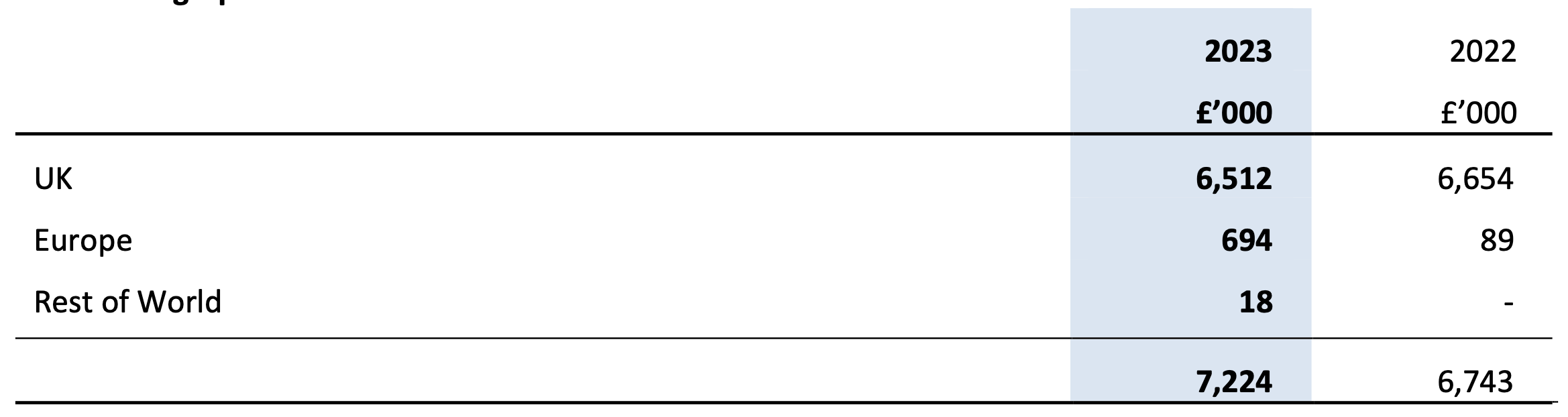

We also see first successes from the expansion outside of UK, especially in Europe and first positive indications, albeit slow, from overseas expansion in US. Sales outside of UK, which will be a key-driver for ongoing revenue growth, crossed 10% of total sales now.

Products

In 2023, Touchstar secured a large 0.25m contract for installing a CCTV system. Based on the news flow published by Touchstar, I assume this was an installation for British Sugar, a client they have been working with for two decades.

Further, Touchstar is looking at the public sector for its access control systems.

We continue to build on accessing Government department requirements and have recently signed up to a government backed portal that provides access to tenders within the national and local government.

Business Drivers

Research & Development

In FY 2023 Touchstar had recorded R&D costs of £972,000 (2022: £1,029,000), of which £583,000 (2022: £565,000) has been capitalised. This compares against Revenues of £7,224 (2022: 6,743) meaning that 13% (2022: 15%) of revenues are R&D costs. This is by no means extreme but still significant.

When we look at the cashflow statement we see that R&D Capex represents almost all Capex spent. Since R&D costs are often associated with growth initiatives like new product development I assume that a certain part of capitalised Capex can be seen as growth Capex.

Expenditures as below could fit to Touchstar’s business, especially considering the note of requiring subcontracted services in FY 23 annual report.

Creating prototypes for new products

Setting up manufacturing processes for individual products

Testing for devices to assure market readiness and compliance

This is actually good news, because if we took an optimistic stance we could add the addition of intangible assets back and significantly increase our calculated Free Cashflow.

For 2022: 1,901 - 60 - 135 - 178 = ~ 1,5m

For 2023: 662 - 17 - 165 = ~ 0.5m (will talk later about the drag from prev. year)

However, R&D can be also focused on improving existing products to maintain competitiveness, ensure compliance with regulations so it can be also seen as sustaining investment rather being purely growth-focused.

And since I want to be cautious in my analysis I will take the pessimistic assumption and stick to the formal definition of FCF which is OCF - (total) Capex.

This gives us

For 2022: 1,901 - 60 - 135 - 178 - 565 = ~ 1m

For 2023: 662 - 17 - 165 - 583 = slightly negative (see Working Capital chapter)

It also needs to be considered that additions of intangible assets are more difficult to value than physical assets so I think it makes always sense to be on the cautious side here.

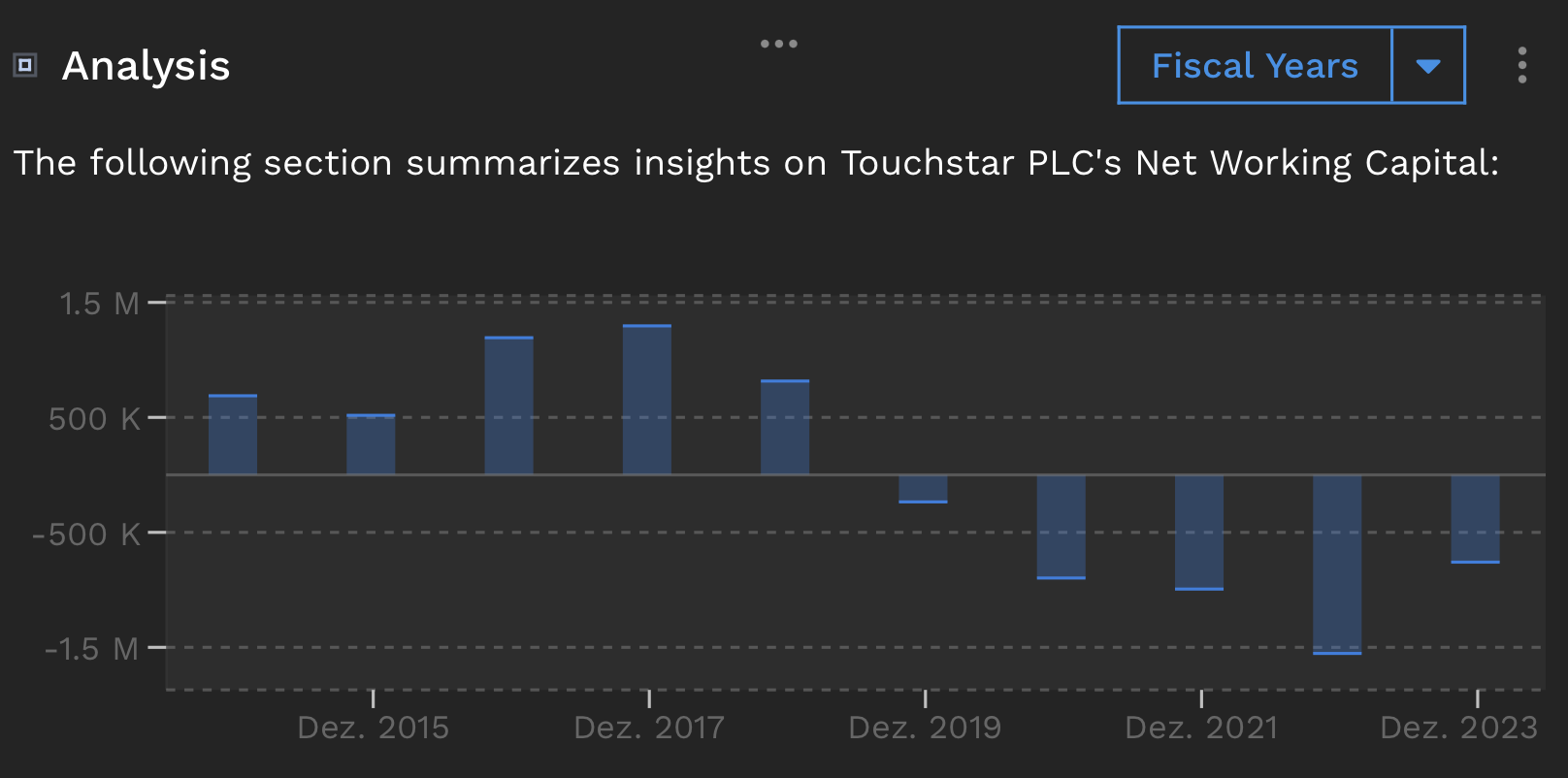

Working Capital

Note how net working capital (Current Assets excl. Cash - Current Liabilities) was negative since 2018, which brought the company in a favourable position.

Even with the positive networking capital change in FY23, working capital is still negative which I really like here. One needs to say that the comps from 2022 were probably hard to beat.

So the reduction in Operating Cashflow compared to FY22 are a Working Capital Issue.

Touchstar made following comment related to a cash reduction of ~0.5m which provides reasons to believe this was more of a one-time thing..

Secondly, a delayed customer go-live date deferred until 2024 and therefore delay in recognising recurring revenue, and thirdly some customer payments received in early January 2024 rather than December 2023.

While I like to see positive working capital changes I don’t consider this to be a serious problem as …

the financials show some fluctuation here which is not uncommon for a company selling niche products which longer replacement cycles like Touchstar does. See again figures below

the company has sufficient cash reserves to cover temporary investments into working capital (FY 2023: ~3m)

I focus on the big picture which remains very solid for Touchstar. See again the operating cashflows and negative working capital in previous years.

Going forward we can assume that R&D costs will slightly increase.

CAPEX spending on R & D is expected to increase again but not to return to FY 18 levels.

In 2018 Touchstar recorded ~0.9m in R&D Capex so I assume Capex of 0.7m going forward is a reasonable assumption. It also shows that the company is reinvesting cash, be it for the sake of staying competitive or growth Capex, it is a good thing as long as it is reasonable compared to cash generation.

Management

Ian Martin (Chairman)

Ian Martin is an experienced turnaround specialist and has proven that numerous times.

This is what Ian Martin has included in his LinkedIn Profile:

I have an established reputation as a strong turnaround specialist, bringing dramatic change to faltering and underperforming companies, restoring profitability, generating cash, embedding control, bringing stability and enabling growth.

However, in 2023 he announced his intention to step down as chairman. I think his role was key for what Touchstone has achieved over the last 9 years so we can only hope that they will find a good replacement.

What is interesting though is what happens with his 10% insider stake. At this moment I can only guess but this is what he mentioned on LinkedIn in the description of one of his previous assignments.

Note: He stepped down in 2012 from Avesco plc

I stepped down from Avesco after 10 years heading the Group although remained the 5th largest shareholder until the business was sold in 2016.

CEO @Acesco Group plc

As CEO of Avesco Group plc (2004-2012), another AIM listed company, he led a significant transformation resulting increasing profits from £2.1m to 12.4m and revenues from £58m to £143m.

Managing Director @Brockbank Group plc

As managing director for Brockbank Group plc (1990-2000), a listed AIM company, he was involved in business activities which prepared the company for a sale. As a consequence the share price rose from £0.85 to a high of £6.96, the price paid by the acquirer XL Capital.

Mark Hardy (CEO)

Taking the description from the website here

Mark joined the company in 1992 and has been involved in the mobile communications market since graduating from University with a BA Honours degree in Business Studies in 1986. Prior to joining the company, Mark worked for American based companies and was instrumental in driving sales of high-tech products into developing markets.

With overall responsibility for the commercial running of Touchstar since 1997, Mark still remains extremely active in the sales and key account management aspects of the business.

Risks

No investment is without risks so let’s highlight some topics that need our attention.

10% Customer Concentration: In FY 2023, one customer accounted for 10% of revenue but management highlighted that they don’t see a risk here with this customer. This is something micro-cap investors see often in small businesses but given the ongoing growth of the business 10% is acceptable in my opinion

Ian Martin steps down, yet unclear who will overtake his role and if he intends to sell his shares which would result in a lower shareholder alignment.

Working Capital Issues in FY23: While it seems like a one-off it is not clear yet what resulted in such a significant change in working capital

Bad Acquisitions: The company announced that a potential acquisition as a use for excess cash is considered. Should that happen we can only hope that it will be accretive for shareholders

I think these are acceptable risks and none of the risks is a dealbreaker for me. The company has done an incredible job over the last 9 years so I think it is unlikely that this reverses due to stupid management mistakes.

Valuation

My valuation is mainly based on the solid net cash position of about ~3m and FCF generation of 0.5m - 1m per year - and a big gift by the market valuing this company at a mere 3-4x EBITDA.

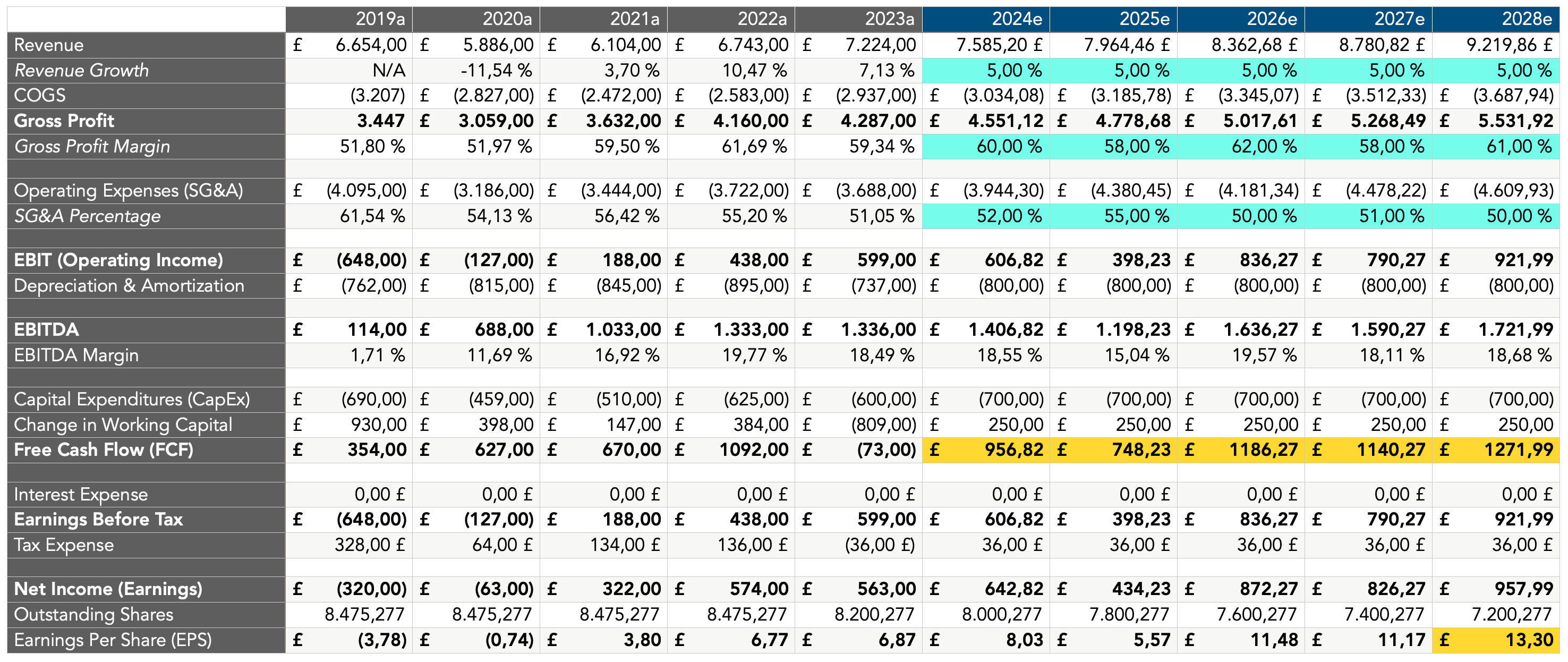

Find below a financial model estimating EBITDA, FCF and EPS for the next 5 years. The following assumptions have been made:

Slow revenue growth of 5% per year which should be rather conservative

Gross margins hovering +/- 60%. Since the company has steadily increased gross margin over the last 5 years (up 10%) I think it is realistic to assume that they can be seen as a consequence of a shift to software and an increasing proportion of recurring revenues

SG&A sitting between 50-55%. Same story here, SG&A has steadily decreased over the last 5 years (down 10%) so I am rather optimistic here while accounting for some lumpiness

I assumed steady D&A sitting somewhere in-between amounts of previous years

Further, I accounted for constant CAPEX at the higher end as Touchstar announced this figure to increase in 2024

While accounting for positive working capital changes (4 out of 5 previous years were positive working capital changes) I kept the degree of change quite low

Since the company has bought back 200k shares in 2023 and budgeted 300k for share buybacks in 2024, I accounted for a decreasing share count of 200k shares every year (quite pessimistic). Today the company could buy more than 315k shares using such an amount. As said, the upside will be realised with share buybacks and dividend payments.

Projection*

*Model is a rough calculation so some numbers from the past don’t add up 100%. The goal of the model was to understand what assumptions I needed to get +100% share price appreciation.

In this scenario which I would consider as a “base-scenario” Touchstar would generate ~5m of FCF so combined with 3m net-cash today, the net cash would exceed the current Market-Cap of 7m.

Everything else being equal Touchstar’s business would then be assigned zero value. I see this opportunity therefore as a low risk, high reward opportunity and acquired shares at an average price of 95 pence.