A Factory delivering 40%+ ROCE (XPF.L)

A Factory delivering 40%+ ROCE (XPF.L)

A stock nobody likes but sites everybody loves

I am not an accredited financial advisor. The content on this substack is my personal opinion and not financial advice. Please do your own research and consult a professional before making investment decisions. If you invest in stocks, consider using limit orders. Invest responsibly.

TL;DR

Enterprise Value: ~£ 54M

Market Cap: ~£ 24M

Free Cashflow: ~ £ 3.5M

Debt: Mostly Capital Leases

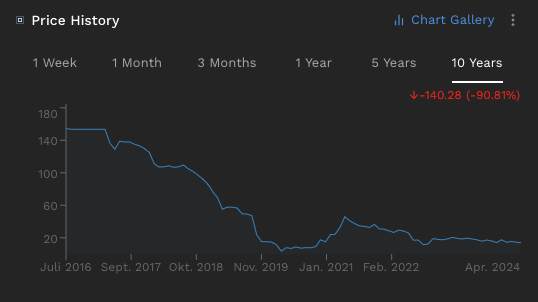

Experience Factory is a UK-based operator of escape rooms and experimental leisure bars, a growing niche in the physical games market. While the stock collapsed nearly 90% since its IPO in 2016, the company became recently cashflow break-even and is poised to grow rapidly.

While the terms “experimental leisure” and “physical games” may suggest an unproven business model doomed to die, I assume the opposite is the case. Their two business segments Escape Hunt and Boom Battle Bars get highest customer satisfaction ratings on Tripadvisor and Google Maps (Google for it!) and have industry-leading unit economics.

While an ever increasing number of people is working from home and spending undeniably too much time in front of screens, I believe that venues focusing on bringing people physically together by providing immersive experiences is a unique value proposition for companies and individuals alike.

The management has set itself aggressive targets and sees potential for 50 more Escape Hunt venues (up from 22) and 100+ Battle Boom Bars (up from 19) in the UK alone. In the near future the company would be able to add 5-8 venues per year from free cashflow which sits around £ 3.5M (FY23).

While the whole restaurant industry faced strong headwinds due to rising input- and labour costs as well as depressed consumer spend, XP Factory outperformed their most-comparable peers by a wide margin, posting double-digit like-for-like growth rates and stellar returns on capital.

Valuation

Meanwhile the stock is trading at an all-time low and sits at ~7x FCF and 5x adj. EBITDA (pre-IFRS 16). If the management hits their targets of doubling their number of Escape Hunt venues and adding more Battle Boom Bars free cashflow is likely to at least double within 5 years.

As the business is operating profitably now I see limited downside at the current valuation. Yet, please consider that cheap can always become cheaper.

The History

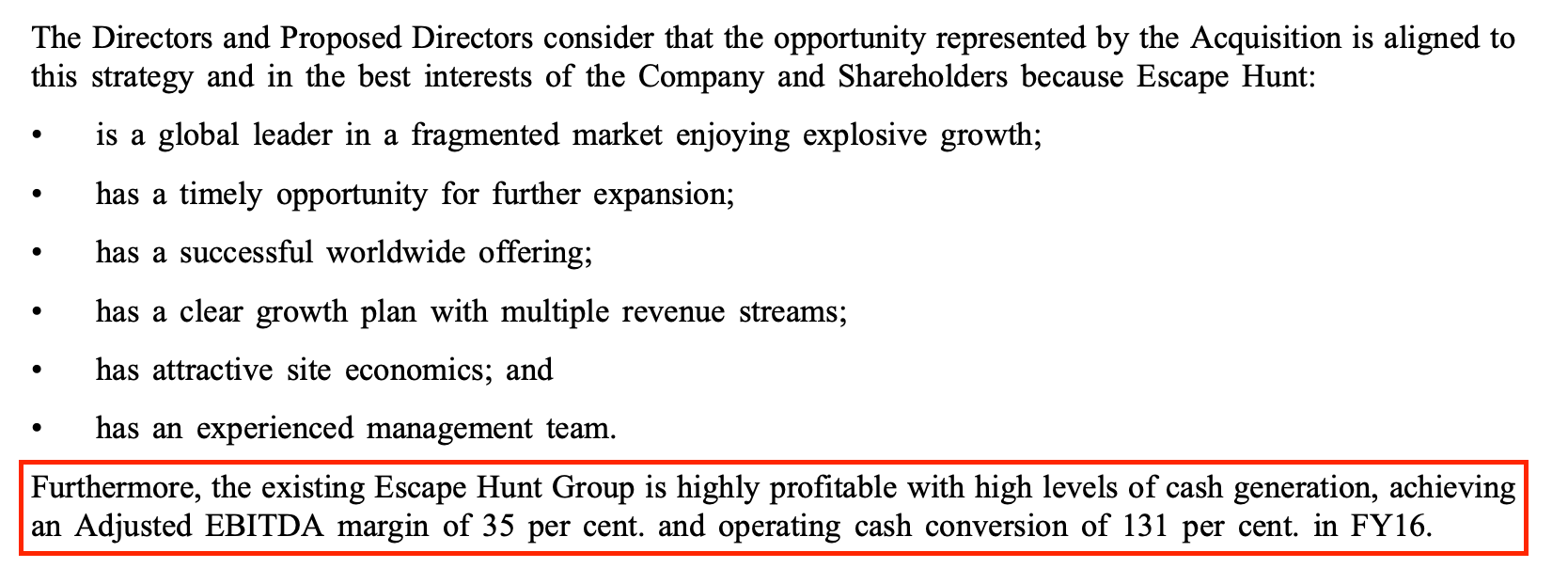

In 2016 investment vehicle Dorcaster Plc IPOed with the purpose to acquire businesses in the leisure sector (Yes, technically a SPAC but don’t run away yet!).

It soon acquired Experiential Ventures Ltd, a global franchisor of escape rooms for a consideration of £7.2 million and rebranded it as Escape Hunt Group.

Find below the rational of the acquisition as noted by the acquirer.

Escape Hunt Group

While the original owner of Experiential Ventures Ltd. acted almost entirely as franchisor with only one owner-operated branch located in Bangkok, the acquirer’s (renamed to Escape Hunt Group) strategy was to open owner-operated stores in the UK whilst also continuing to franchise and sub-franchise internationally.

UK Opportunity for Escape Hunt Group

Similar to the global market, the UK market is fragmented, as only a handful of operators have more than four branches. Furthermore, the majority of these operators operate branches with only one to three rooms per branch, while Escape Hunt Group planned to generate more capacity by fitting five to six rooms into one site.

For people still wondering what an escape room really is, find an explanation below:

An escape room is a physical adventure game in which players are typically locked in a themed room and have to find clues and solve puzzles in order to escape against a countdown clock. Escape Hunt games typically require players to solve a crime story or mystery, which has been tailored to the location of the branch, within 60 minutes.

Escape room games are enjoyed by a variety of people from gamers to families, tourists and friends. Increasingly, corporates use escape room games for employee assessment, management training, leadership evaluation and team building.

Game Design

Escape Hunt Group had created over 250 different onsite and offsite games of varying styles and applications. Every game goes through a 32-stage design process and is customised to the specific requirements of the location. Depending on the requirements, ‘EH Magic’ is specifically built-in. EH Magic is the technology used in some of Escape Hunt’s games which manages music, lighting, actions caused by puzzle outcomes, remote monitoring and game master interaction outside the room via CCTV, speakers and microphones. It is designed in collaboration with the Escape Hunt’s technology design supplier based in Thessaloniki, Greece.

Site Layout

Escape Hunt Group’s branches offer spacious lounge areas which enable après-game team building or entertainment. Furthermore, the branches offer a ‘mini-theme park’ experience, offering refreshments, dressing up for souvenir photos and sale of Escape Hunt merchandise. It also aims to employ and train friendly and professional staff who can offer guidance to customers throughout the experience. Comments made by TripAdvisor users on Escape Hunt regularly cite Escape Hunt Group’s staff as a key component to their highly positive experiences.

The spacious locations make Escape Hunt venues also to an ideal place for corporate events, like team building and training activities. These services have been provided to a number of blue-chip customers.

Richard Harpham, CEO of XP Factory, said in an interview that when setting up Escape Hunt venues in the UK it was very difficult to get sites in prime- and high-street locations. This is because landlords didn’t know what escape rooms were and there was only a small niche of people visiting such venues.

Surviving Covid

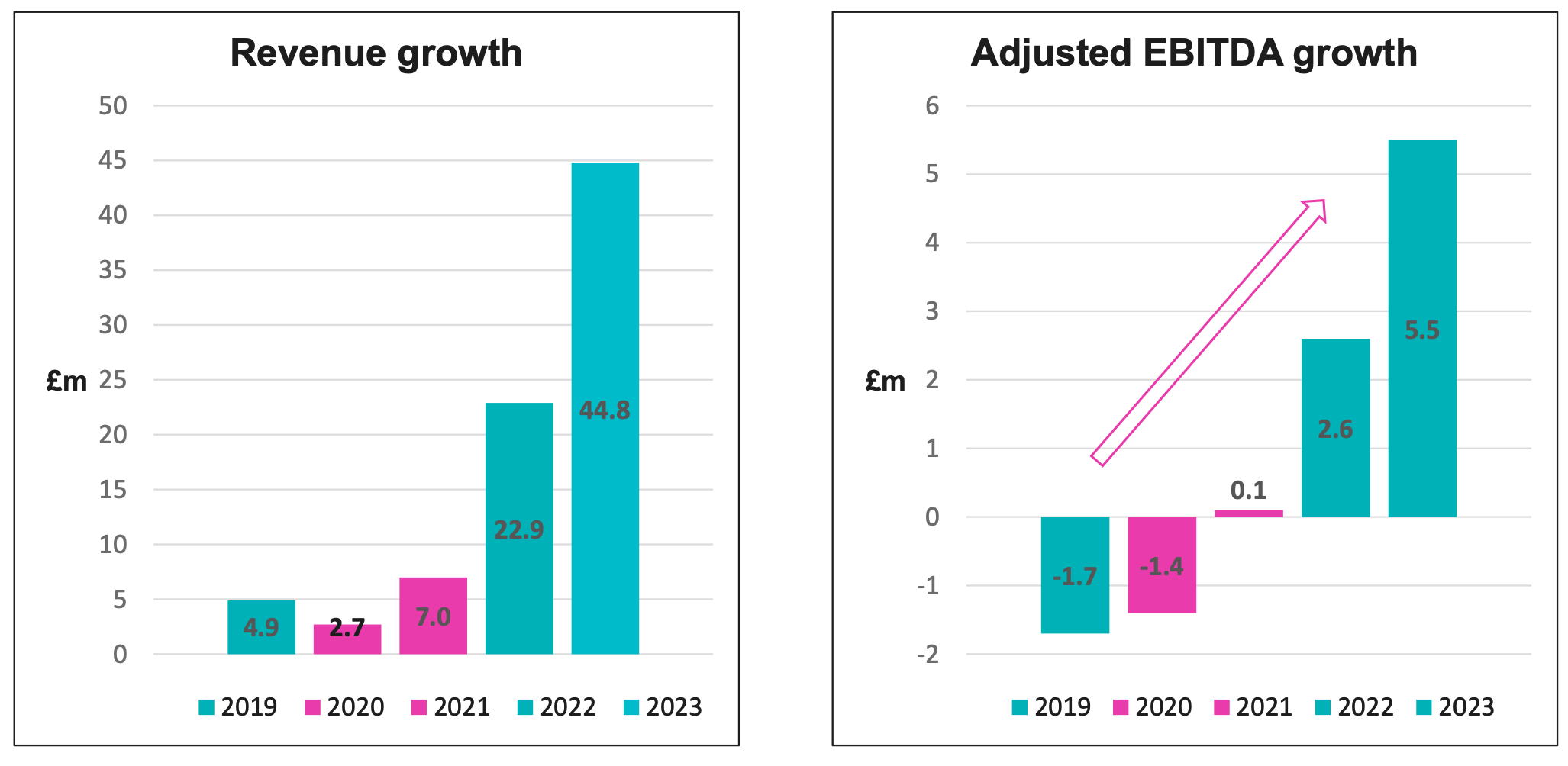

When the pandemic hit in 2020, XP Factory had a mere 5 million in sales, were still loss-making because lots of initial capex was spent and the sites were at an early stage of their respective maturity curve just to get closed during Covid.*

*This compares against impressive 45m sales and 5.5m adj. EBITDA today.

XP Factory had to take a risk.

This is what Richard Harpham said about it in an interview:

“We placed it all on black if you like. We decided to go hell-for-leather after this property market, to make the most of the landlord insecurity that existed for the first time, and to try and grow.”

During Covid, when many investors doubled down on growth stocks, XP Factory doubled down on the property market by securing 8 more sites for Escape Hunt effectively doubling the number of sites in a single year.

But that’s not it. XP Factory made another bold decision.

While 3.000 sq ft units were still in high demand after Covid, 10.000 sq ft units were not. They were 50-60% cheaper and landlords would make contributions to get them sold. But there was a problem. The company could not fill this much space with venues like Escape Hunt, which required much less space.

This is why … you guessed it … XP Factory acquired Boom Battle Bars in 2021. As the group operated two separate units now, the group renamed from Escape Hunt Group to XP Factory, an analogy to “Experience Factory”.

Boom Battle Bars

I am not sure if you are open to learn about the other competitive socialising business of XP Factory after reading my bits on Escape Hunt Rooms, but I can promise that Boom Battle Bars have a great value proposition.

Imagine a bar with loud music “Boom” where you have also the chance to “Battle” with your friends with axe lanes, darts, shuffleboards, mini-golf, augmented reality. Add on top some cocktails and street food and you are good to go.

Richard Harpham explained in several interviews how well Escape Hunt venues and Boom Battle Bars augment each other and smooth out earnings over the year.

While Escape Hunt Rooms are often visited during vacations by families late in the evening or on weekends, Boom Battle Bars are visited by adults (well it’s only for adults) after-work in the normal course of the year with capacity being less filled during vacations. This adds enormous value to the run-rate of sales over the year and reduces cyclicality in the business.

Unit Economics

Richard Harpham promoted in the earnings call that the focus lies on "box economics” meaning site economics and its constituent parts.

He outlined also what a healthy business looks like:

Strong ROCE (EBITDA / Capex net landlord contributions) for sites being open for 1 year

Strong LFL growth

It is important to understand that LFL growth tends to be higher when sites are not mature as the revenue growth rate is higher for younger (immature) sites. So the 29% for Boom and the 17% for Escape Hunt as posted for FY23 won’t be maintained for forever. Think about it like this: The higher the proportion of immature sites, the higher the potential LFL growth and vice-versa.

Good conversion to cash by taking adj. EBITDA (pre-IFRS) as a proxy for Cashflow.

The company generated about 6.2m operating cash converted from 5.5m EBITDA. Now deduct some maintenance Capex and interest payments on leases and you get 3.5m Free Cashflow to be spent on new sites.

Sound customer reviews

Escape Hunt

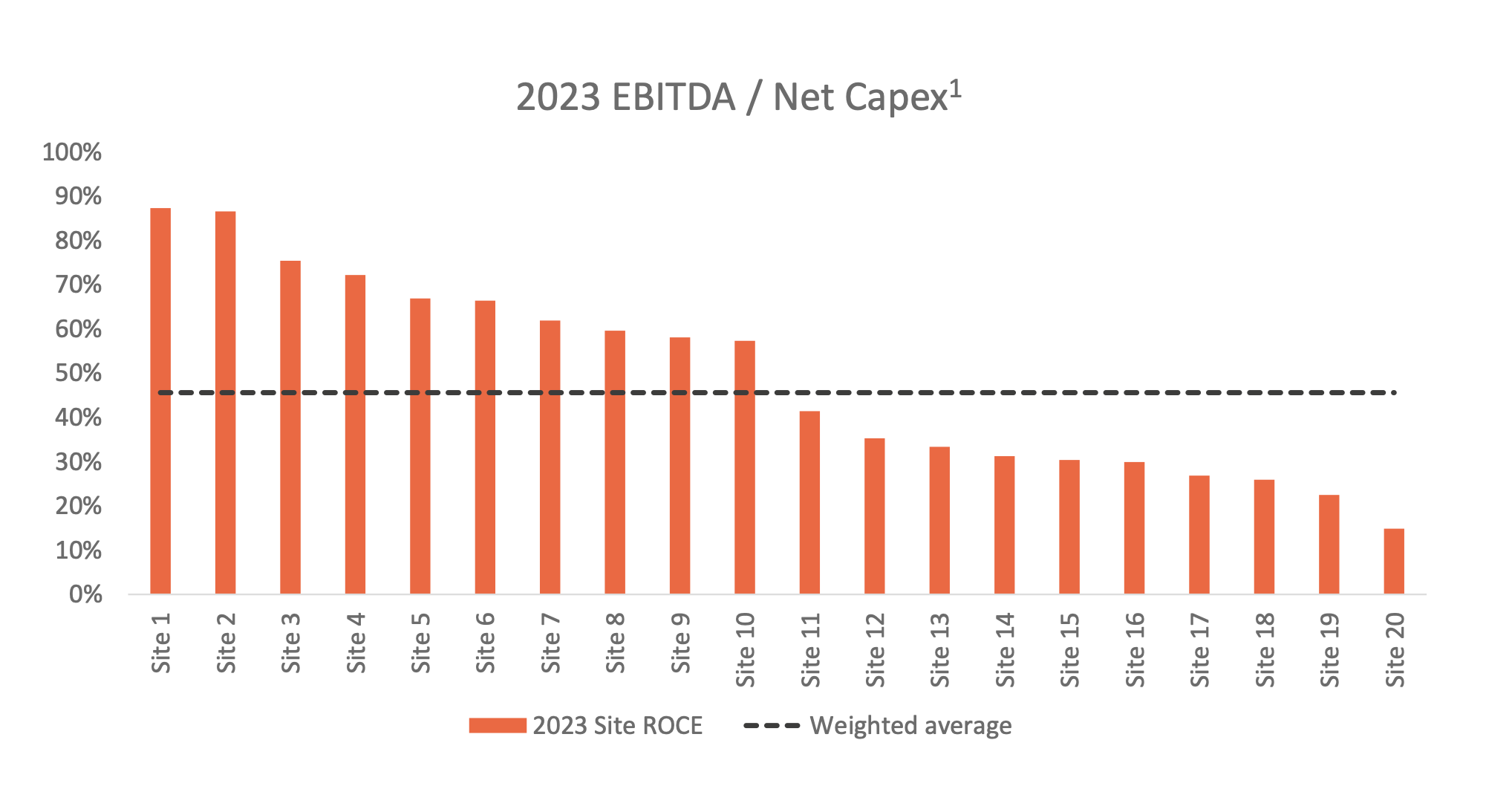

I took this slide from the investor presentation and want to highlight some dynamics behind the return on capital employed (ROCE) for Escape Hunt.

The slide maps the ROCE for the 20 owner-operated Escape Hunt sites. The higher the ROCE, the quicker the payback on the site acquired.

What we can see here is that some sites have an exceptional high ROCE up to 90%, some sites hover around 40% and some other sites have a ROCE below 40%. The average ROCE sits around 45%.

The confusing thing about this slide is that it tricks us into thinking that each site added has an incrementally lower ROCE than the site before (caused by the ascending numbering of sites from left to the right). This would be a dying business then.

Yet, as Richard Harpham explained in the last earnings call, the opposite is the case. ROCE has increased over time as learnings could be drawn from openings meaning the representation is a bit misleading (the numbering).

And this makes sense. Imagine you open a fast-food restaurant for the very first time. Maybe you pick an unfavourable location or spend too much time planning so that the opening is behind schedule. Maybe you onboard also low-performing staff or you don’t get the menu right. Most likely you don’t get landlord incentives either because landlords are sceptical about your business and your brand is still unpopular.

So the important take-away here is that you can flip the slide around as the ROCE has increased over time.

We are a cornerstone for shoppingcenters […]Landlords typically like us. Sites that we achieve today are materially better than we achieved four years ago.

"We've seen it transform in every regard in terms of its economics, which are now very much industry-leading: 20% like-for-like sales growth, 40% EBITDA, and 50-something percent return on capital. I would describe it as something of a crown jewel in the experiential leisure.”

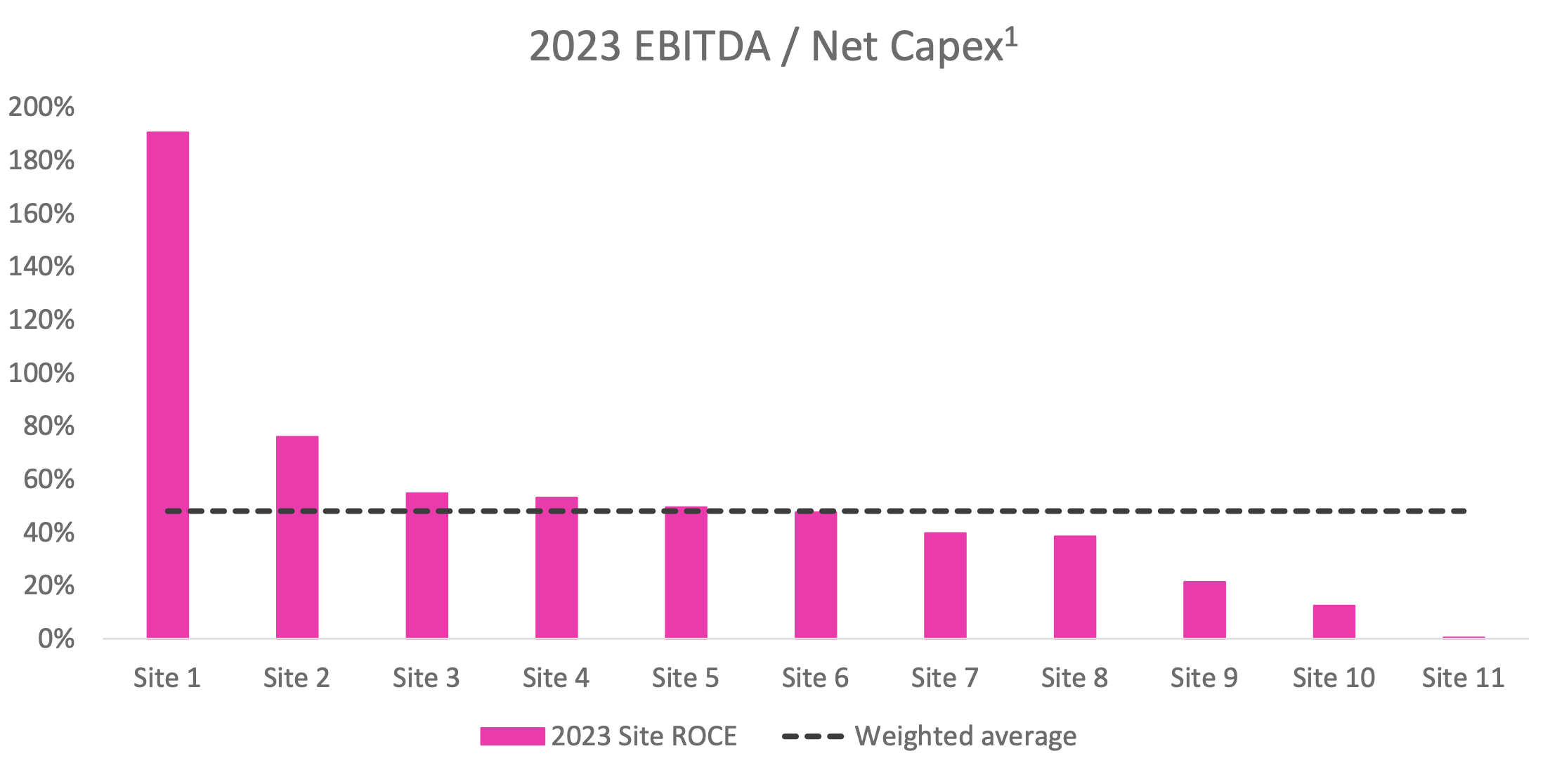

ROCE Dynamics

Yet, what the slide still does not tell us is what sites are represented by each bar and how the maturity profile impacts the ROCE. This is because over time, as sites mature, the ROCE should increase as …

more revenues are generated as sites are more popular

more EBITDA flows through as revenues increase and incremental Capex decreases

There are also other factors, let’s call them one-off factors …

Some sites have been acquired cheaper relative to their earnings potential (retrospectively)

Some sites simply perform better (more traffic, better locations)

Richard Harpham also confirmed in the earnings call that over time we can expect ROCE to increase further for sites currently sitting below the line.

Site Economics

You may wonder how much it costs the company to refresh games. While the strong, still double digit LFL-growth from original sites (that are 6 years old!) does not indicate that a refresh is due, it needs to be considered at some point.

New games developed for Escape Hunt are actually readily available and would just need to be deployed. Thereby the supplier uses a modular approach which facilitates the transfer of games between locations.

Fitting in a new modular game from scratch costs 50k while the transfer of a modular game from one location to another location is estimated to cost around 15k. As I understood, the Dubai site opened in 2023 is a pilot for such modular games which will then be reinstalled in sites in the UK in some years. They call it “content rotation”.

Richard Harpham pointed out that Escape Hunt is a low Sales, but high Margin business.

So let’s assume build Capex for an Escape Hunt is 600k. A ROCE of 45% means that on average a venue earns 270k EBITDA a year after opening. Since EBITDA margins are around 20%, we get a revenue of 1.35m.

We discussed already that installing another game may cost 50k for each room. So if we take 5 rooms per Escape Hunt venue we get 250k every 5 years or 50k per year which is ~4% of revenues. Note that I took the pessimistic assumption of non-modular games. Should modular games reduce maintenance costs to 15k per instalment, savings would be significant.

Boom Battle Bar

Boom Battle Bar is the nascent business acquired in 2021. One advantage of this business is that it has a high value for landlord as it increases the attractiveness of the surroundings. For this reason landlords will often grant landlord contributions.

Boom Battle Bars are a higher Capex but also higher Revenue business with similar margins, resulting in a similar ROCE.

Currently, EBITDA margins for sites being open for at least 1 year is a solid 18% while target is 20-25% Site EBITDA margins for Boom.

Initial Investment: ~ 0.9m

60% = Site Infrastructure

40% = Game Installements (0.36m)

Maintenance Capex

Accounts mainly for Game installments every 3-4 years

0.36m/4 (years) ~0,1m

Annual turnover: ~2m

% Growth Capex = 50%

% Maintenance Capex = 5%

EBITDA margin = 20% (0.4m)

Return on Growth Capex: 0.4m/0.9m = 44%

Valuation

Let’s crunch some numbers based on FY23

Growth investments for Boom net landlord contributions and new investments (in acquisitions) we get about 7.5m Capex

5.2m adj. EBITDA (pre-IFRS) need to be adjusted for 1.6m EBITDA contributed by new acquisitions and give us 3,6m adj. EBITDA which can be considered as good proxy for OCF in the long-term

ROCE = 3,6/7,5*100 = 48%

So let’s say we reinvest those 3,6m FCF at a 40% ROCE.

Note: Consider that I don’t calculate a present value but simply take a reasonable multiple on FCF which is a simple approach that I am able to understand.

Further, I assume that there are only mature sites which is not true. So in reality there is 1-2 year time-lag to achieve the 40% ROCE. As I would need to do a complex calculation based on number of stores open in each given year, I decided to do a quick calculation as below.

FCF 2027: 3,6*1,4*1,4*1,4 ~10m

Market-Cap at 5 x FCF: 50m (100% upside)

Market-Cap at 10 x FCF: 100m (400% upside)

And this is just for 2027 which is a glimpse away. I won’t make a long-term projection here because I think they are inherently risky and unforeseeable. This is why I prefer strong growth and high return on capital at a reasonable valuation as it provides a quick payback on my investment with low risk of permanent capital loss.

But what I can tell you is that compounding at this rate for 6-10 years would achieve incredible returns on an investment today. And while long-term projections are risky and unforeseeable, they are actually very easy to make on this simple business. The determining factor will be ultimately the ROCE over time. Can they maintain it? I have no idea, but they have really executed over the last years.

Market & Competitors

XP Factory operates in the food & beverage (F&B) industry but also in a niche called “competitive socialising”. While the term competitive socialising as such is still very unpopular I made some research and discovered that it is actually emerging in the UK and US.

As F&B pure plays are highly competitive, competitive socialising provides a way to differentiate your venue from others. While the initial value proposition is centered around food and drinks, the attractions make them stand out.

Competitors

There is a wide range of venues that can be considered as a competitor but I think for XP Factors it is much more difficult to come up with comparable peers because they are quite unique. Further “competitive socialising” is quite the new kid on the block.

I could shortlist the following competitors based on my research.

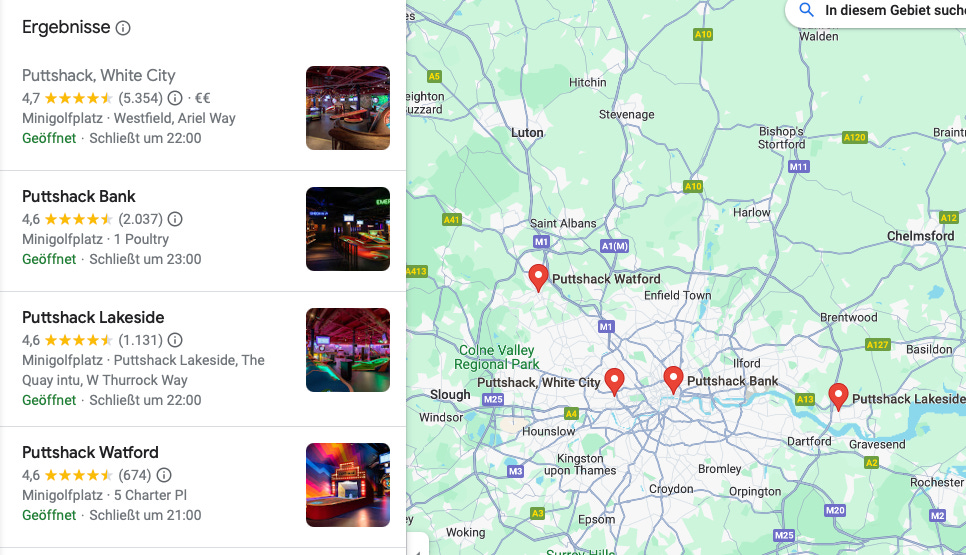

Puttshack: F&B + Minigolf

Flightclub: F&B + Darts

F&B Pure Plays

Leisure Pure Plays (i.e. Attraction parks, cinemas, etc.)

It is interesting to see that various providers of competitive socialising venues get excellent customer ratings across sites so that I believe that the ratings are not just based on factors like service in that specific site but also on the concept itself (which is an incredible advantage for any business, it’s basically good reviews for free).

This is actually a good thing, as customers often look at ratings on google maps when they decide where to go to. A Boom Battle Bar or a Puttshack has a better rating than a local burger restaurant? Well, then let’s go there and play some mini-golf besides having food.

I really like the unique value proposition here.

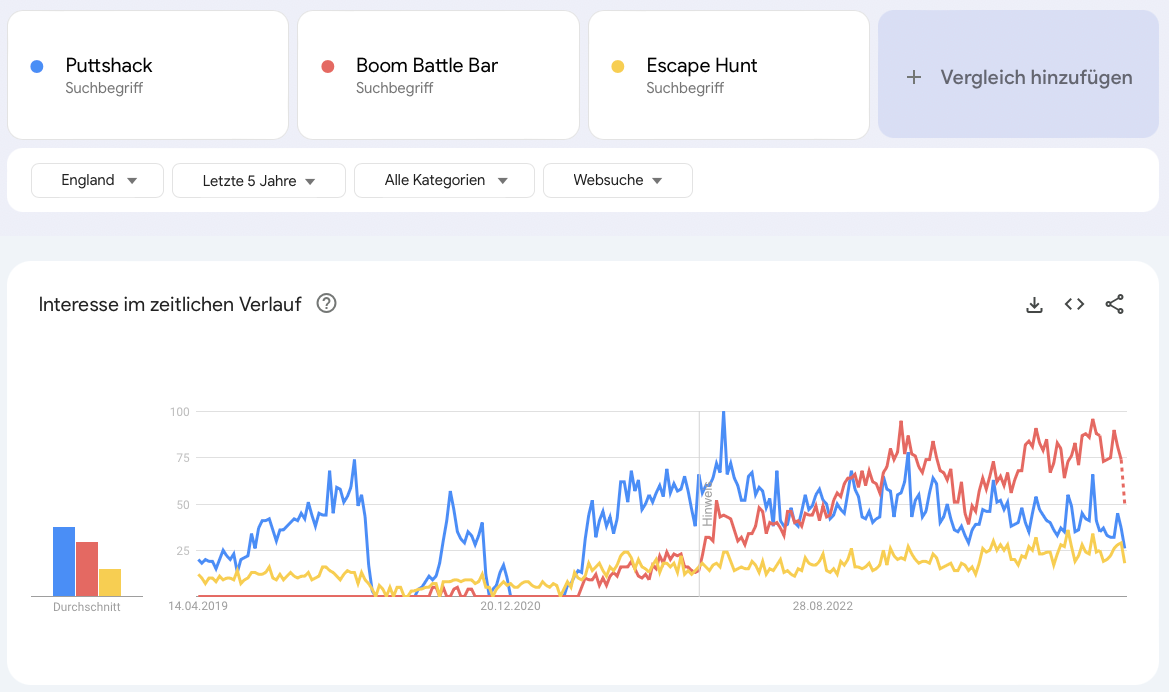

I was surprised to see that you can actually see a strong trend for various competitive socialising venues in the UK.

While Escape Hunt can be seen as steady performer, it is interesting to see that Boom Battle Bars outperformed its peers including Puttshack. One explanation I came up with is that Puttshack is more “premium” than Boom Battle Bars making it more difficult to fill capacity in inflationary times.

Richard Harpham pointed out many times that they managed to keep prices steady by adding capacity rather than increasing prices.

Is competitive socialising a secular trend (Skip, if not interested)

When I had a look at the wider leisure industry and niche blogs / magazines I was surprised to see how much is happening lately in the field of competitive socialising. Let me give you some impressions about emerging concepts in this space.

BattleCart, NL: ~30 venues, expanding rapidly

Drive around an incomparable Playground: Different circuits, bonuses and game modes are projected directly onto the floor, allowing you to interact with the scenery and other players. Full throttle aboard a electric karts to live a supercharged experience!

Larks, US: 2 Locations, +6 planned

Welcome to Larks, an eatertainment venue, cocktail bar, and a chef-inspired restaurant where shuffleboard is king and nostalgic games live alongside state-of-the-art fun for all ages.

Swingers, US: 6 Locations, UK and US, no info about expansion

Swingers, the crazy golf club, has reinvented mini golf for an adult audience by adding gourmet street food, cocktails and a party atmosphere.

Chicken N Pickle, US: 11 Locations, no info about expansion

We cultivate a vibrant, inclusive community, where families, friends and colleagues can create memories and connect through playful experiences, delicious food, and shared celebrations in a playful backyard setting that fosters human connection and support for our neighbors.

BigFangCollective, UK: 6 locations, no info about expansion

Our concept combines seriously crazy golf, cocktails, DJ’s and Street Food in an art infused environment that showcases the very best street art, its writers and its culture. We always love to remind people……

Lane 7, UK: 9 Locations, +8 planned

Venues as unique as their host cities. Find your nearest Lane7.

Roxy Ball Room, UK: 18 Locations +2 planned

Roxy brings the playground to the bar, with a huge variety of games all under one roof, and massive rock and indie tunes. Whether it’s date night, mate dates, overdue catchups, work parties or just Booze and Ball Games, Roxy has you covered!

And much more …

My Take

Although I am far away of being a Macro-Guy, I find the emerging concepts interesting. They target much more space (10k sqm), they target a whole bunch of people (groups of friends, families) socialising together, they are a perfect fit for corporate customers and they are somehow fundamentally different to all those concepts we know already (Cinemas, Food, etc.).

For this reason they have also different economics, less rent per square meter, higher cross-sell opportunities and more capacity utilisation.

What I believe is that the global shift to home-office increases demand for such venues. What people tell me and what I experience myself is that when you go to office, you almost don’t go there to work anymore. You just talk to your colleagues you haven’t seen for a while. Years ago this was different. Everybody worked hard to “look busy” in the office.

My current employer has scheduled an on-site team-meeting once in a month in the evening to revive the connections which simply go lost by sitting at home all-the day. And guess what we are talking about? Bowling, participating in a cooking course, Paintball, and much more.

People are looking for experiences more than ever before.

Management

In this section I want to talk a bit about management and what I like or dislike.

Focus on return on capital

Richard pointed out several times that the return on capital is the ultimate metric for the business going forward. As a consequence the group focuses not on opening this or that number of new sites per year but how quick an investment returns capital. And this is exactly what I would describe as “shareholder-oriented”.

He explained it like this: If adding capacity to existing units or buying back franchise sites generates a higher return on capital than adding new sites, they will go for it. In order to identify high return of capital opportunity, they collect a lot of data for every venue. If a third Shuffleboard or third Axe-lane does not cut it, maybe crazy golf does. They have a dedicated roles in their company (I found the guy on LinkedIn) doing such analytics. And to be honest, I haven’t heard about other companies doing such sophisticated analytics.

For instance, they replaced meeting Rooms in Escape Hunt venues with new game rooms. Or they will swap a game room which is underperforming by another one.

Another example is that in the Boom Battle Bar in the O2 tower, they realised that most visitors planned to visit a concert and therefore did not register for games at the Boom Site. So the company invested an additional 250k into a cocktailbar (People love to drink before going to a concert) and this investment brought a sales uplift of 15k per week providing a payback on investment within 6 months.

I like the opportunistic mindset here. And as covered in this article they don’t just talk about it, but have demonstrated this opportunistic behaviour already during COVID and through their acquisition of Boom Battle Bars to benefit from high ROCE sites.

Focus on owner-operation

Richard also had a clear opinion on their strategy for franchising. While the company is in a good starter position for franchising having master franchising agreements for many countries in place, he said that the largest opportunity to capitalise on is currently owner-operating venues in UK. Richard said they were approached by many individuals who are eager to bring this concept into the US and France but they think for now it makes more sense to focus on the larger opportunity.

As franchising is done internationally but

is a minor part of revenues today and ..

is not considered a key-focus of the group currently, I did not cover the franchising economics in this write-up but will detail things out should this change in future

Focus on the customer

Customer centricity is a buzz-word promoted by many businesses. XP Factory is no exception here. Yet, looking at customer reviews for Escape Hunt and Boom Battle Bars and comparing them with those of other venues in the leisure segment, the focus on customers pays its returns.

While reviews for Escape Hunt are still a tad better (not to say outstanding) than Boom Battle Bars, one needs to consider that Boom Battle Bars is also more challenging to manage.

Higher and quicker turnover, more games, factory-style operation, less staff for a higher amount of people, less structured. Despite those challenges, they are doing it incredibly well.

Imagine you have put 1m into an Escape Hunt venue and you get rated below 4 stars on Google Maps. Would customers still visit this venue or try to find an alternative? I guess site economics would significantly be impacted as there is a significant amount of fixed costs which can only be covered by filling capacity. So going after each and every negative review is an absolute high return on capital decision. During my research I was wondering how bad this "easy quick win” is handled by most restaurants.

Risks

Let’s look at some risks we need to consider.

Low-Insider-Ownership

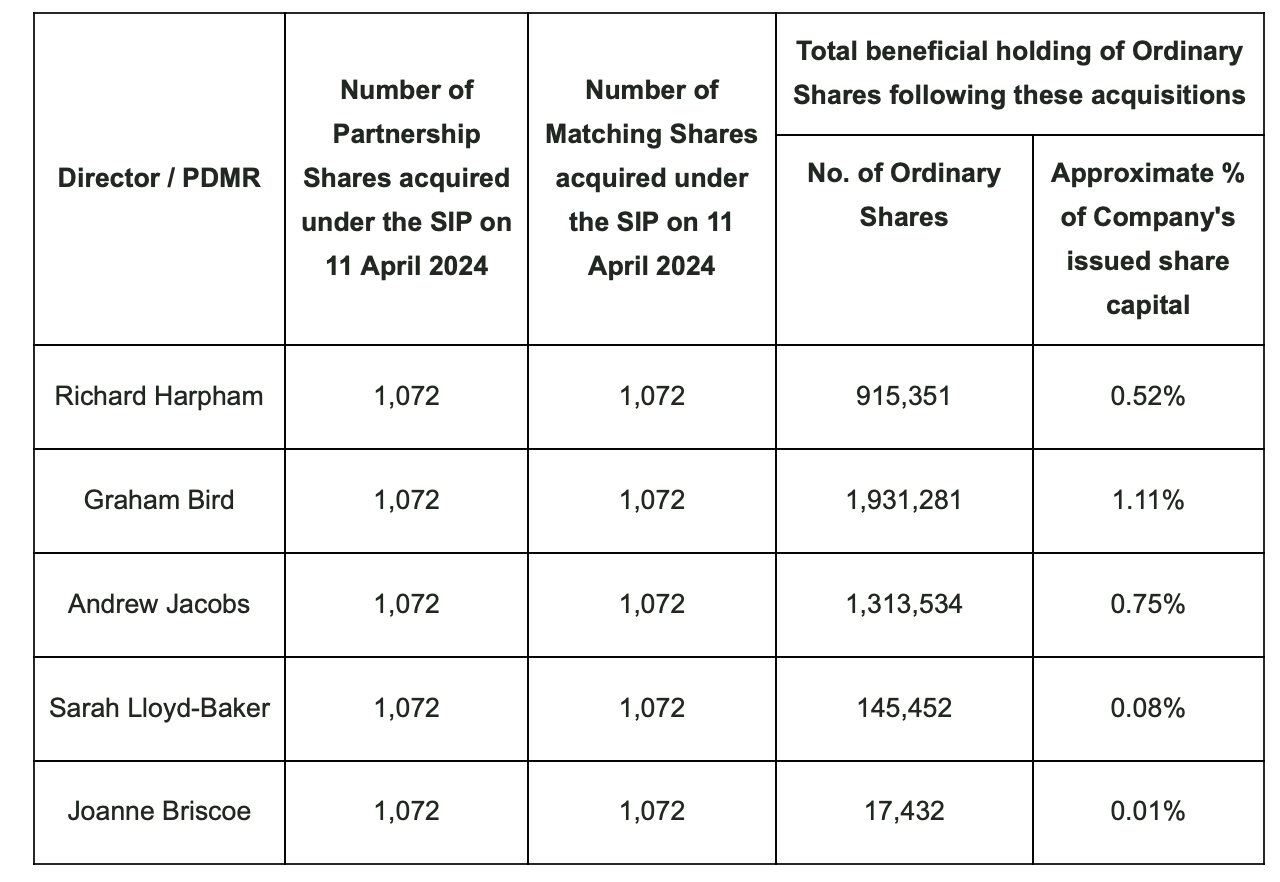

This is something I couldn’t wrap my head around and is the main anti-thesis if you want so. Richard Harpham holds a mere 0.52 % of outstanding shares which does not result in a good shareholder alignment.

Yet, Andrew Jacobson (COO) bought 410.53k shares over the last 12 months at an average price of UK£0.16.

While there a good performing businesses with low insider ownership and also bad performing businesses with high insider ownership I like to see skin in the game as it gives me trust in my investment decision.

However, insider ownership may not be seen just as percentage of total outstanding shares but also compared to the actual net worth of holders. Find below the current value of holdings.

Richard Harpham (CEO): ~140k

Graham Bird (CFO): ~280k

Andrew Jacobs (COO): ~180k

While I have no idea about the individual networth of these people I think the actual amount of holdings is not too bad.

High goodwill

The company has 21m goodwill (see explanation below). Since goodwill is not a real-cost as it is already paid it is more about valuation in terms of replacement value. If something goes wrong there is not much left-over. You can’t sell goodwill to anyone.

Escape Hunt

I have played an escape hunt game with former working colleagues and know that it is fun. It is just difficult to see where this concept stands in 5-10 years from today. Is it a fad at some point? Or will it be incremental part of socialising activities in years to come? I don’t know. I am only pretty sure that competitive socialising is a huge theme and confident that people will like to spend time together aside from virtual meetings. Yet, what we can see is that even original games being installed for more than 6 years now still demonstrate solid LFL growth and that venues belong to the top attactions of their surroundings. So why not being optimistic here? Beside that, I focus on a reasonable/cheap prices in business so that I don’t need do 5-10 year projections anyway.

Dilution

The company has diluted in the past and despite its profitability it wouldn’t surprise me if they acquired another competitive socialising business in the future. The company is a real execution machine but also very ambitious and I hope they will allocate capital wisely and don’t overspend.

Conclusion

So how do we value this opportunity? If we take the stance of a value investor, looking for acquisitions priced at. 2-3x EBITDA, XP-Factory threw money out of the window. Accounting for dilution caused by share considerations at low stock prices the acquisitions were even worse.

Battle Boom Bars was acquired for 17.38m in 2021 and delivered ~7.1m adj. site-level EBITDA in 2023. While this is not too bad it needs to be considered that at the time of acquisition only a handful of physical sites were acquired - the remainder was goodwill. So it was actually more like the acquisition of a brand.

Escape Hunt was acquired for 7.2m in 2016 and delivered ~6.4m adj. site-level EBITDA in 2023. Same here, there was only one owner-operated site at this time so most of the Capex spent was not included so it was a brand acquisition.

Yet, it is important to see where we stand today. After years of cash burn and significant shareholder dilution, I believe the company with the recent results from FY 2023 to be significantly de-risked from further dilution and capable to deliver +40% returns on capital by simply executing on the opportunity to replicate their successful venues across the UK and internationally.

It ticks most boxes I am looking for in investments

Single digit FCF/adj. EBITDA multiple

High revenue growth

You can model/project the business well

Good Capital Allocation

(Kind of boring business) > I find it quite exciting tbh but not an issue unless this is priced into the stock

Replicable, just about execution less about genius decisions

(High Insider Ownership) > not fulfilled

Do your own research, this is no investment advice. I hold a position at a price of 14,50p.

Under competitors, I wood dig into Redwheel. There has been strong noises from the over the past year to aggressively expand in the UK.

And then there are entertainment players like Gravity (see Gravity Wandsworth for an example) that are closer to BBB - multiple games all in one place for "activity based indoor social outings".

Great thesis! I will look into it for sure. Regarding skin in the game, have you looked at incentive plans? Does the company have any share-based long term plan?